Can you beat the market with this bankruptcy predictor?

Using the Altman-Z score with a little twist.

Hi everyone,

It always surprises me that so many investors are putting their money in ETFs/Index Funds, being at the mercy of market whims, when in reality there are dozens of strategies one can use to gain a slight upper hand. You don’t need to be a stock-picking genius to beat the benchmark, instead, think about it this way:

Don’t search for massive profits. Search for 2-3% outperformance per year. Do this 10 years in a row, and you will see massive profits.

I introduced to you in previous articles two easy-to-use ratios that have historically rewarded those who used them:

In today’s issue, we are going to focus on downward protection by using the Altman-Z Score that helps us to spot companies that have a bankruptcy risk. Successful investing is more often about avoiding dull stocks that drag your portfolio down, instead of finding tomorrow’s superstars. Even a portfolio of average companies will do the job as long as it doesn’t contain big losers. But how can we easily spot dangerous stocks? There isn’t one ratio that can give you 100% certainty, but backtests over many years still provide valuable information if a method works more often than it doesn’t. So let’s take a look at today’s ratio.

The Altman-Z Score

The Altman Z-score is a multivariate formula for measuring a firm's financial health and a valuable tool that estimates the likelihood of a company going bankrupt. According to studies on the efficiency of the Z-Score, the model has an 80%-90% accuracy in predicting bankruptcy within the next two years of operations. This approach employs five financial ratios that are combined in a specified manner to yield a single number. This number, known as the Z score, is a broad indicator of a company's financial health. Since it was first introduced in 1986 by Edward Altman, it has been slightly developed and adapted to be applicable to a wider range of companies (because originally it was developed for manufacturing companies). In this article, I will introduce you to the original version so that you can better understand how this ratio works.

The classic Z-score model is based on five different key figures that are weighted according to fixed factors. The following key figures form the basis of the Z-score:

Working capital / total assets (1)

Retained earnings / total assets (2)

EBIT / total assets (3)

Market value of equity / liabilities (4)

Sales / total assets (5)

These key figures, weighted with the corresponding factors, result in the following formula:

Z=1,2∗(1)+1,4∗(2)+3,3∗(3)+0,6∗(4)+1∗(5)

For a comprehensive understanding of the z-score, the key figures that are used play a crucial role. Depending on their evaluation factor, they are weighted differently in the final result. The five key figures are explained below and the focus is on their suitability for insolvency forecasting.

Understanding the Altman-Z Score

Working capital / total assets (1)

A company's working capital consists of current assets minus current liabilities. It therefore represents the capital that is tied up in the company in the short term and is used for the production of products or services. For a company, low or negative working capital means the risk that short-term liabilities cannot be serviced without difficulty. Conversely, high working capital can indicate that a company is not operating effectively. High inventories, for example, tie up capital that could just as easily have been invested in the company's growth.

Retained earnings / total assets (2)

Retained earnings represent the net income retained by a company. Companies reinvest their retained earnings back into the business, often for capital expenditures, acquisitions, but sometimes also to pay off debt or hold extra working capital. Altman also defined this ratio because it takes into account the age of a company. The longer a company has been in existence, the longer it can build up its retained earnings, assuming profits. At the same time, companies with a long history tend to be considered less at risk of insolvency.

EBIT / total assets (3)

This key figure is a gauge of a company's productivity. Earnings before interest and taxes (EBIT) are divided by the company's total capital. This shows how much profit a company generates depending on its capital. Typically, high values of this ratio are viewed positively by investors. This ratio is particularly relevant for forecasting a possible insolvency because it reflects a company's earnings power. The higher a company's earnings, the lower the risk of no longer being able to meet liabilities such as supplier invoices or interest payments. A high EBIT-to-capital ratio therefore tends to reduce the risk of insolvency.

Market value of equity / liabilities (4)

In the event of a company liquidation, the company's liabilities must be covered by assets. As long as the ratio between market capitalization and liabilities is positive, this can generally be assumed. A high equity value in relation to low liabilities also suggests financial stability.

Sales / total assets (5)

Investors can use this ratio to derive how much revenue a company can generate with each dollar of capital. However, a high turnover only has a positive effect if profits can be generated from the turnover. For this reason, this key figure has a significantly lower weighting in the Z-score.

What is a good and a bad ratio?

Altman defined three different zones in his scoring model. Below a value of 1.8, a company's insolvency risk is greatly increased. Between a value of 1.8 and 3.0, companies are not acutely at risk of insolvency, although there are already negative indicators. Above a Z-score of 3.0, a company's insolvency risk is low.

Keep in mind that it shouldn’t be used as a standalone ratio for short-selling (the Ohlson-Score for example has a higher accuracy), but more to avoid companies with financial distress. When used correctly, it could save you from big headaches. I will cover in future articles other bankruptcy predictors that can be used as a team to find short-selling candidates.

The good this about this ratio is that you don’t need to do the calculations yourself each time because most stock screeners already include it. If you want to test it for free, I can recommend gurufocus for a good overview simply because they provide historic data for this ratio. One year can be exceptionally well or bad, so better take a look at the whole picture to see if a company is operating generally well. This source covers many stocks for free. (Note: This article is a general introduction to this ratio, there are two other slightly different adjustments to the Z-Score which I will cover in a future article).

Can we find outperforming stocks with the Z-Score?

Alright, now comes the interesting part. If a low ratio signalizes risk of financial distress, then a high ratio leads us to financial stability which should serve as a basis for long-term performance. By using simple logic and this ratio we should easily be able to spot stocks we want to own and stocks we want to avoid. Let’s take a look at two random examples. Keep in mind that a stock that has consistently a low Z-Score won’t make you any money because financial health is the cornerstone of stock performance and vice versa. One great compounder over the last decade has been Home Depot HD 0.00%↑ , here is an overview of their score:

Impressive, not once were they in financial distress according to this ratio, and on top of that their average score is 6.8. Of course, many other factors play a role in the performance of a stock, so I wouldn’t use this as a standalone ratio but as another checkbox that gives us in combination with other factors a ranking we can use to make better investment decisions. Here’s how this stock performed:

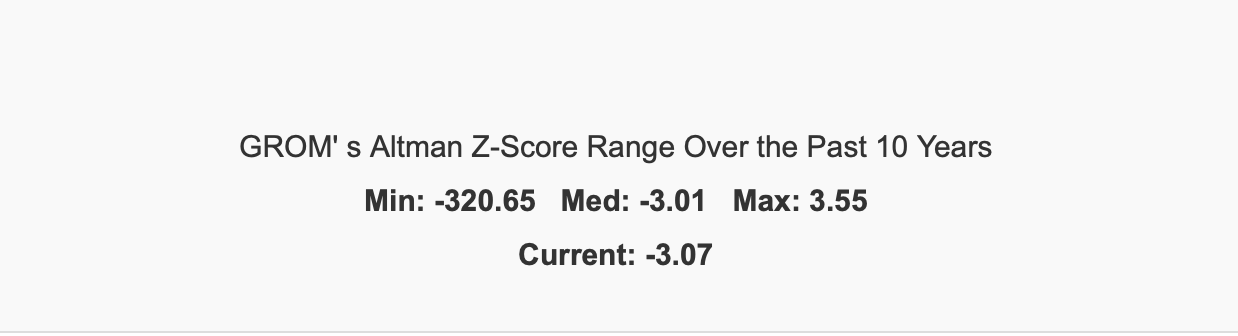

Now, what does the extreme opposite look like? How would a stock performs whose Z-Score is constantly in the negative? One of the worst performers that I found is Grom Social Enterprises GROM 0.00%↑:

If you see this, just stay away and avoid the headaches.

Of course, some luck or survivorship bias can’t be excluded, but as I wrote in previous articles, start making investment decisions based on odds and probabilities. With a high score it’s likely that you have found a great performer and vice versa.

Last but not least

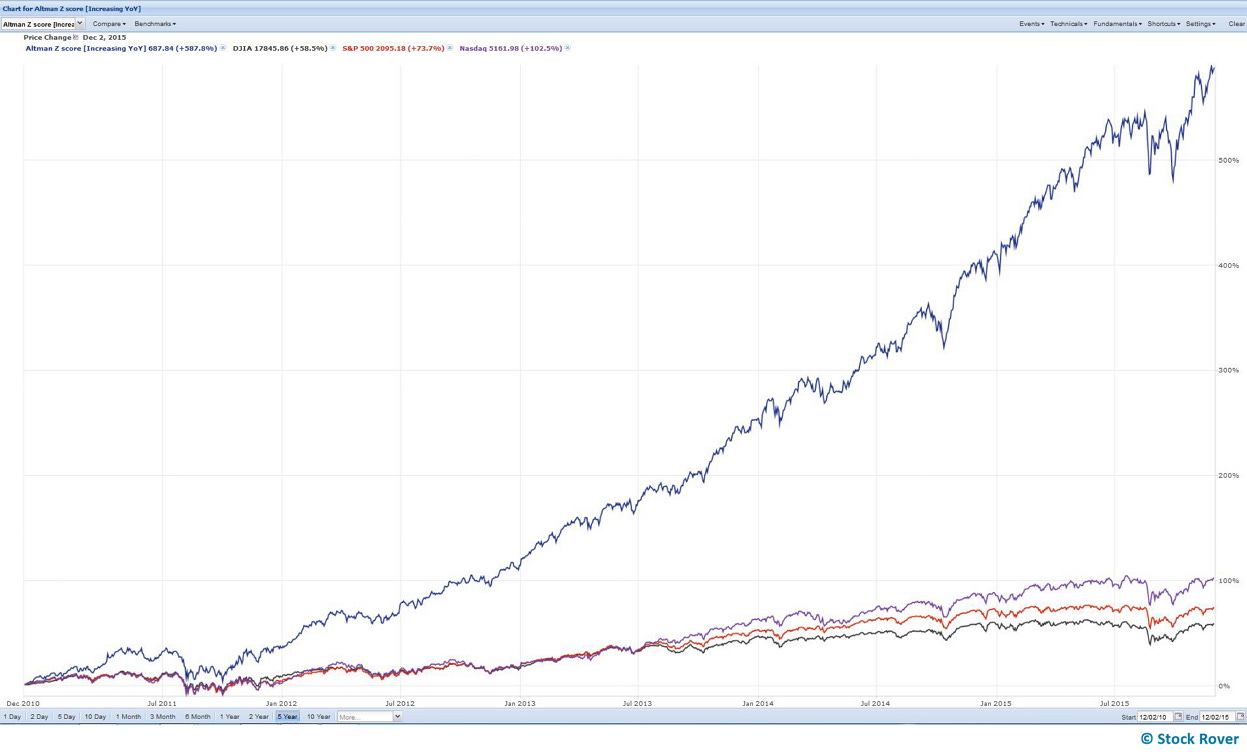

From my experience, I observed that Wall Street loves above all else an improving story. A company that is executing constantly well will lead to a higher share price step by step. But a company that is making jumps in its performance will give you more gains in a shorter time period. Just think about turnaround situations. You have a company that is on the brink of a collapse, then they get a new manager who cleans up the mess of the previous one, and the share price jumps at the first sign of hope. The same happens when a company improves its already good performance. With this in mind, I found an interesting backtest: The increasing Altman-Z Score.

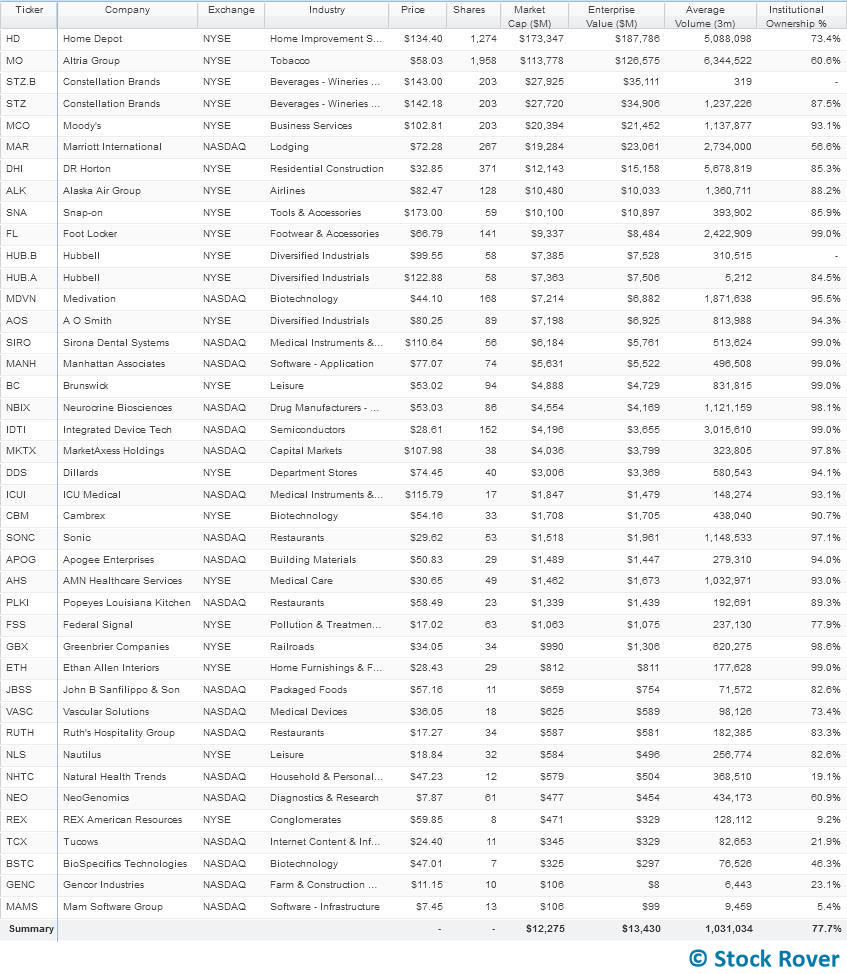

What would happen if we found stocks that not only have a Z-Score above 3 but that have had an increasing Z score every year for the past 5 years? The backtest is from 2010-2015 and contains 39 U.S. companies named below that fit those criteria.

The results (blue line) are impressive when compared to the benchmarks:

Sure, this is a backtest and hard to replicate but nevertheless, it tells us that keeping an eye on increasing Z-Scores can lead us to tremendous profits.

Final words

The Altman Z-Score is a great metric for measuring the current financial health of a company and determining the odds of that company going bankrupt in the near future. Firms that have Z scores greater than 3 are unlikely to go bust and can be a great choice for long-term investors. You don’t need a ratio that will give you 100% accuracy, you just need a reliable toolbox that you can use to make better investment decisions, and the Z-Score is a useful addition. A Buffett quote sums this up perfectly:

“It is better to be approximately right than to be precisely wrong.”

I hope you learned something today. Until the next issue. 👋