Dart-throwing monkeys vs. Cathie Wood. Who wins?

How probabilities can work in your favor

Hi Everyone,

Most of you know the famous stories about monkeys who select random stocks by throwing darts at a newspaper's financial page and coincidentally those stocks perform just as well or even better than the picks from most professionals.

Where is this coming from? It began in 1973 when Princeton University professor Burton Malkiel claimed this in his bestselling book, A Random Walk Down Wall Street:

From that point on, the story of the “dart-throwing monkeys” spread across financial magazines and fed the narrative that the stock market is just a giant casino (which is true to some degree). Of course, journalists don’t want to ruin a good story with facts, so let’s see if it’s true and what we can learn from it.

We are going to examine this from two angles:

Would dart-throwing monkeys outperform the experts, and if yes, why?

Why do so many experts underperform?

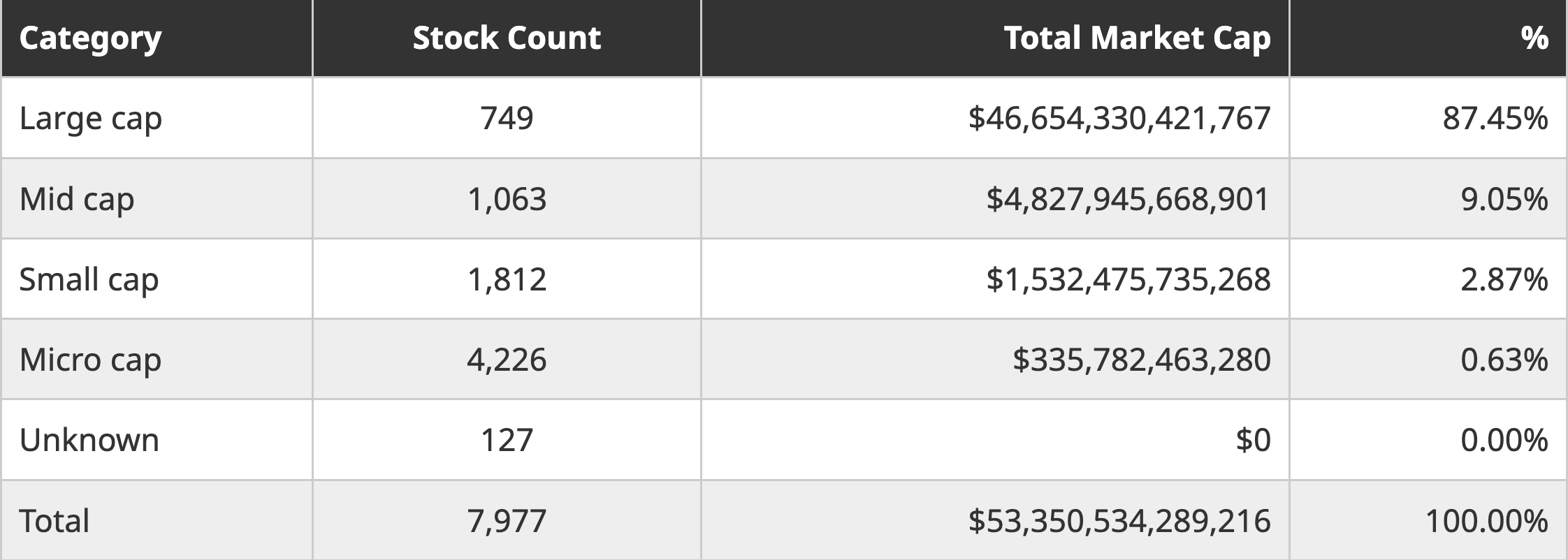

Let's begin with a mental exercise. Consider that you have a dartboard. All publicly traded U.S. stocks are evenly distributed on this dartboard. To avoid overcomplicating matters, 8,000 U.S. stocks are utilized (the actual number depends on the source and counting method; some companies have multiple tickers for example).

Now we are throwing 100 darts and constructing a portfolio with 100 stocks. The holding period is secondary, but let's assume we hold them for three years. Does this portfolio have the potential to outperform the majority of institutional investors? In short, yes, the odds are in our favor.

To comprehend this, we must examine the compositions of this random sample. These stocks are listed below by their market capitalization:

Readers who are familiar with factor investing can guess where this is going. For those who are new to this investment style: Factor investing is an approach that aims to capture the returns associated with certain characteristics (factors) of a security or group of securities.

Factors are attributes that have been shown to be related to investment performance. Some examples of commonly studied factors in finance include for example the value factor (cheaper stocks outperform expensive stocks), and the size factor (smaller stocks outperform larger stocks).

As you see, we have a very large pool of small-cap and micro-cap stocks on our dartboard. Most money managers are limited regarding the pool of stocks they can select from. It’s not uncommon that companies need to have a specific market capitalization to be considered for a fund because smaller companies are considered riskier or because a fund is simply too big to invest in small companies.

In addition to that, we have two tailwinds with small caps that benefit us: Better value (because they are often overlooked) + more room to grow. That means that by simply choosing from the “better” pool of stocks, we already have the probability on our side.

As you see, there is no trick or smart monkey, it’s all about smaller company stocks and value stocks outperforming the market over time. Something that appears like random stock picks is not random at all because of the pre-selection that raises the probability of picking promising stocks. Any portfolio of 100 stocks randomly selected from the list of 8,000 stocks is bound to include mostly smaller companies.

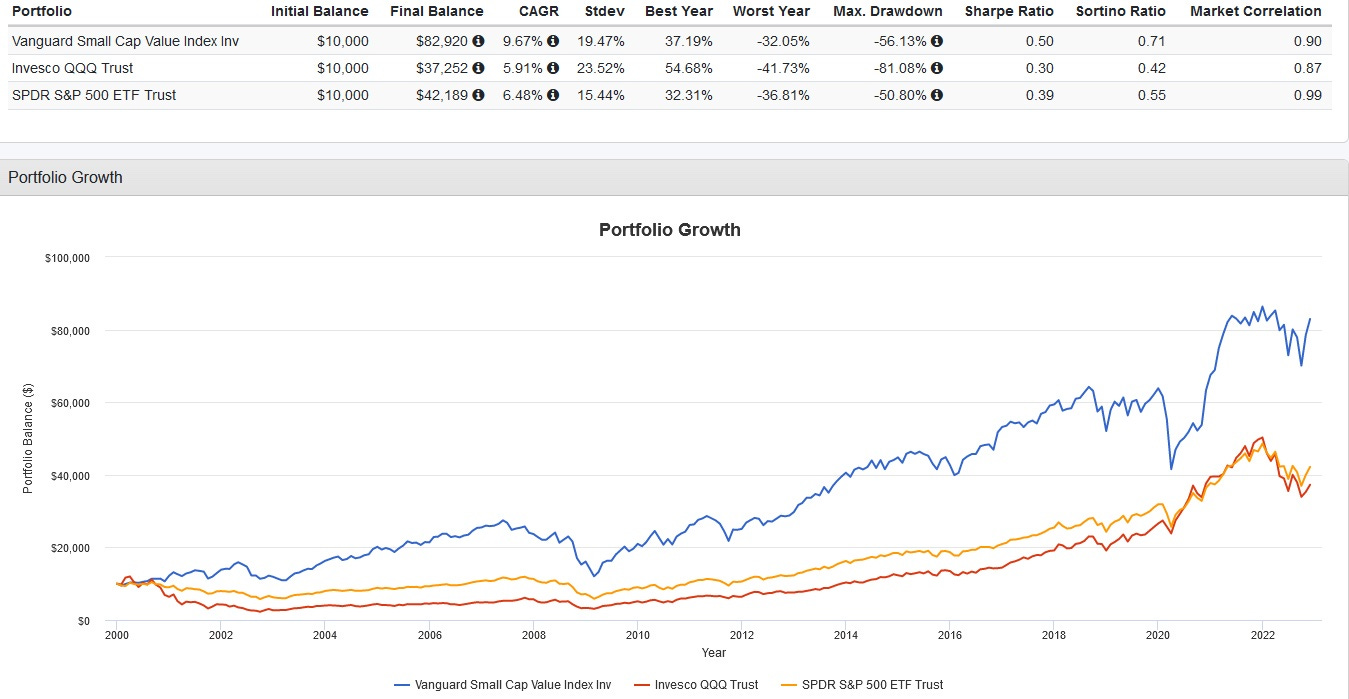

And if you combine factors like size + value, you get impressive results over time. Here’s an example from Vanguard’s Small Cap Value Index:

Last but not least, our "random" portfolio is equally weighted (which means each stock gets the same amount of money invested). What appears to be a random byproduct gives us an additional advantage. Equal weighting increases our exposure to smaller stocks relative to market capitalization weighting. It is as simple as that.

Why do so many professionals underperform?

Now let’s get to the second angle.

Unquestionably, certain active asset managers are in a league of their own. To outperform the market takes a number of qualities that the majority of investors lack. But the reasons why so many underperform are various. I want to focus on two of them which are connected.

As contradictory as it may sound, a significant portion of stock market success is doing nothing. You choose the right company for a reasonable price, and then you wait and let the company do the work. Fund managers are usually expected to submit monthly/quarterly reports and face performance pressure from their investors. But how reasonable is it to expect results within three to six months?

A quarter is meaningless, and a year is sometimes not informative either. This leads to avoidable missteps. I am aware that concepts such as re-balancing are common in the investment community, but I believe it’s a mistake.

Consider the following: Who do you think is more capable of multiplying money over time? An experienced management team, or you, attempting to outwit them by trading in and out? I prefer to choose the most qualified company and let them do the job.

The psychologist Daniel Kahneman sums up the next problem better up than I could:

“The person who acquires more knowledge develops an enhanced illusion of her skill and becomes unrealistically overconfident.”

Overconfidence is what we see all the time on Wallstreet. The “big ideas” of stocks, financial media is full of this. If you are too overconfident, you will struggle to admit your mistakes and learn how to do it better. But as counterintuitive as it may sound, this is what is being looked for on Wallstreet:

“Experts who acknowledge the full extent of their ignorance may expect to be replaced by more confident competitors, who are better able to gain the trust of clients. An unbiased appreciation of uncertainty is a cornerstone of rationality - but it is not what people and organizations want. Extreme uncertainty is paralyzing under dangerous circumstances, and the admission that one is merely guessing is especially unacceptable when the stakes are high. Acting on pretended knowledge is often the preferred solution.”

Final thoughts

Analyzing the dart-throwing monkeys on a meta-level reveals a valuable lesson. Although the monkeys are unaware, statistical probability is simply on their side, giving them an advantage. This has nothing to do with the common journalistic trope that the stock market is a casino.

It can be a better strategy when investors don’t focus on “this one stock”, but instead learn to take a step back and learn how probabilities can work in their favor by selecting from the right pool of stocks in the first place.

Here is a previous article where I explain one way how I view probabilities when it comes to selecting stocks:

I hope you learned something today, and if you aren’t a subscriber yet, subscribe below.

Until the next issue. 👋