Is Intel Stock a Buy Right Now?

When Was The Time To Get Out?

This publication is free (and will stay free in its current form). But if you find value in it, feel free to show your support with no more than the cost of your favorite coffee:

Dear Investor,

The short answer to the headline is: No.

Here’s the long answer:

Intel's INTC 0.00%↑ stock has plunged nearly 59% year-to-date, driven by a series of unfortunate developments. The decline was largely fueled by weaker-than-expected earnings in the last quarter, the suspension of dividend payments, and announced plans to cut jobs in order to fund a major overhaul of its chip manufacturing division—an effort that is part of Intel's $10 billion cost-reduction strategy.

Analysts view these cost-cutting initiatives as the company’s attempt to turnaround its chip-making business amid dwindling profits and market share.

As I looked into it to see if investors could have avoided such a financial disaster, I was struck by how many investors seemed to miss the warning signs. It’s surprising that so many ignored the critical importance of Free Cash Flow—the lifeblood of any business that underpins everything from revenue growth and dividends to product development, share buybacks, and acquisitions.

A closer look at the financials, particularly the inflow and outflow of cash, would have shown that trouble was on the horizon.

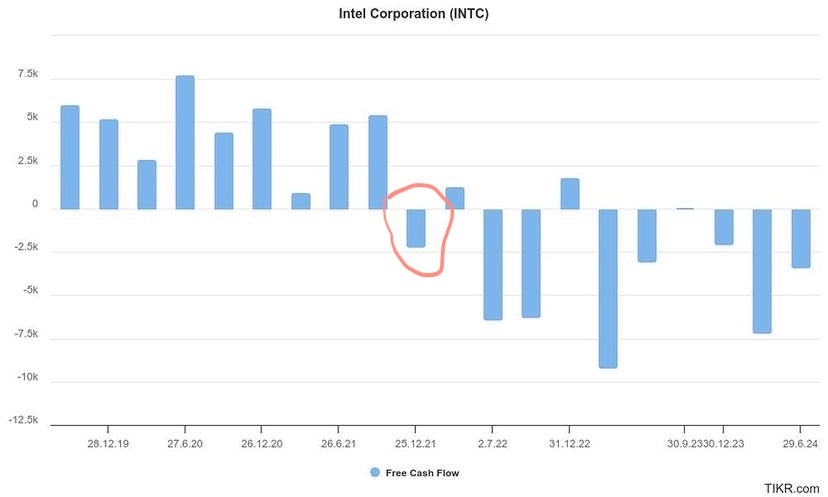

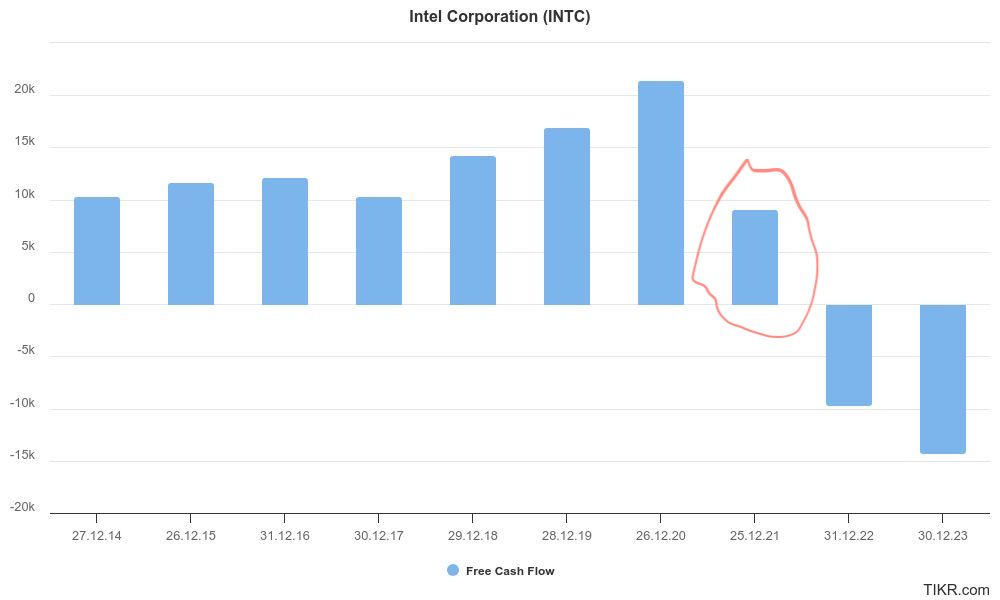

With that in mind, let's examine Intel’s Free Cash Flow for each quarter over the past five years.

By the end of 2021, the first major warning sign emerged: Intel began burning more cash than it generated, with a deficit of $2.23 billion. Just two quarters later, it escalated into a full-blown crisis, with a staggering negative Free Cash Flow of $6.43 billion. Attentive investors would have noticed that the Free Cash Flow in the earlier quarters of 2021 was already significantly lower compared to 2020, as you can see in the graph below.

It fell to less than half of the previous year's level, though it remained positive. While this alone might not be a reason to give up on the stock - it could be a one-time event -it should certainly catch the attention of any prudent investor and be a reason for further investigation.

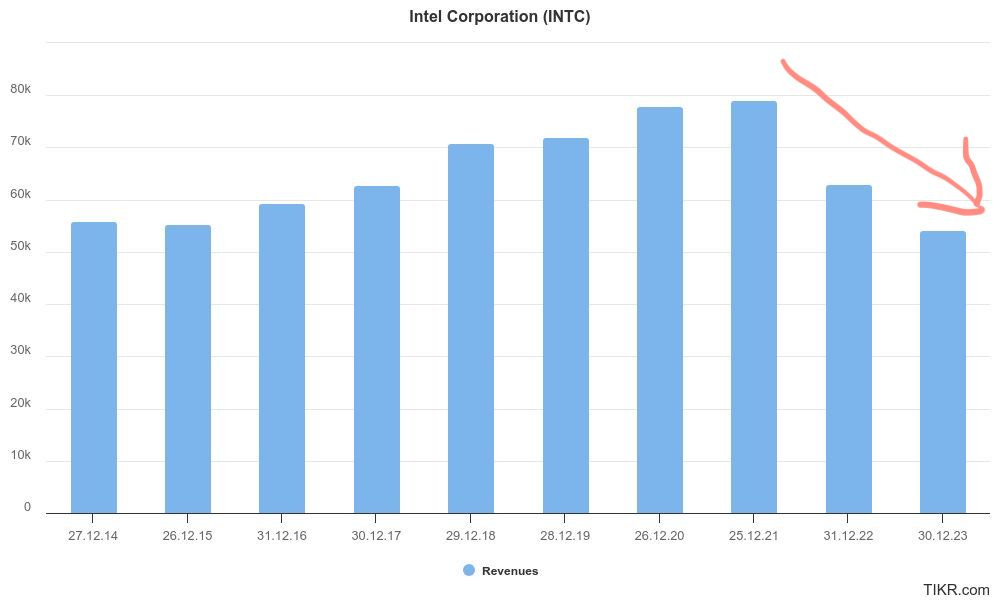

Combine this with a decline in revenue (a metric Wall Street values highly), which began its downturn in 2022, and you have a recipe for disaster.

If investors had focused on the hard facts, such as Free Cash Flow, rather than analysts' estimates, market potential, A.I. hype or other secondary factors, they would have recognized the warning signs in 2021 and potentially exited their positions.

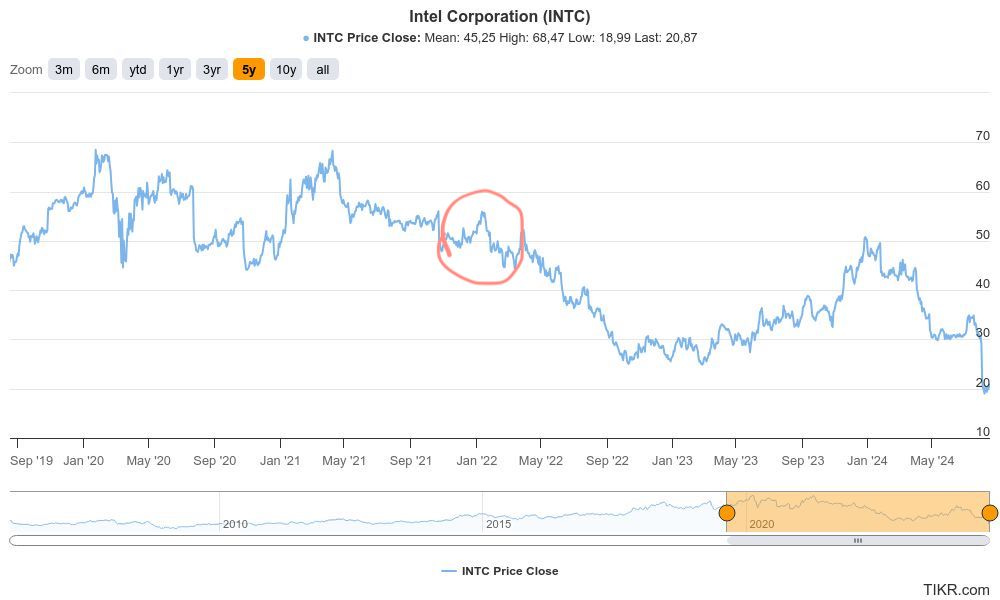

At the end of 2021, the stock was trading around $50 when the first quarter of negative Free Cash Flow occurred.

Even if investors had bought it at a higher price just a few months earlier, it’s always wiser to accept a 10-20% loss rather than allowing a catastrophe to unfold and finding yourself down over 50%, all while clinging to hopes of a recovery.

Which bring us to the headline:

Is Intel a buy right now?

Intel currently falls into the speculative "turnaround opportunity" category rather than a stable buy-and-hold investment. Valuing such volatile companies is challenging, as performance can vary wildly quarter-to-quarter.

Investors who prefer predictable "business as usual" stocks may want to avoid Intel for now. Without reliable free cash flow projections, it's difficult to determine if the current stock price is attractive or overvalued.

How are you going to value a company that is volatile in its financial performance? One quarter it starts burning cash, the other quarter it seems like there’s light at the end of the tunnel and the next quarter the hole just gets deeper.

If you have no idea what to expect for next quarter’s or next year’s free cash flow, you can’t possibly value the business.

If you can’t value the business, you can’t know whether or not the stock price is attractive or horrendous.

If you don’t know what to think of the stock price, you can’t comfortably and confidently own a piece of the business.

In my view, because Intel's stock has been severely beaten down, any positive news could trigger a sharp rebound in its share price. We saw a similar reaction recently with Starbucks SBUX 0.00%↑ when their stock jumped 20% after announcing that Brian Niccol, CEO of Chipotle CMG 0.00%↑ , would be taking over as Starbucks' new CEO.

However, investing based solely on news is usually reactive—by the time you act, the news has already been priced in. On the other hand, investing based on fundamentals and earnings calls allows you to get in early, as many on Wall Street tend to overlook the numbers and focus on headlines instead.

Therefore, I would monitor Intel over the next few quarters to see if Free Cash Flow normalizes and becomes sustainable.

You've just read about Intel's woes. Now, let me introduce you to a company that's everything Intel isn't.

In a world obsessed with flashy tech giants, one company quietly dominates its niche - and could dominate your portfolio.

While the market chases the next big thing, savvy investors are zeroing in on a software powerhouse that's been hiding in plain sight.

This isn't just another stock. It's a financial fortress that:

Generates high free cash flow like clockwork

Offers a unique value proposition protected by law

Has weathered economic storms for decades

Delivers consistent results day in, day out

Imagine owning a piece of a business so essential, so well-protected, that it practically prints money.

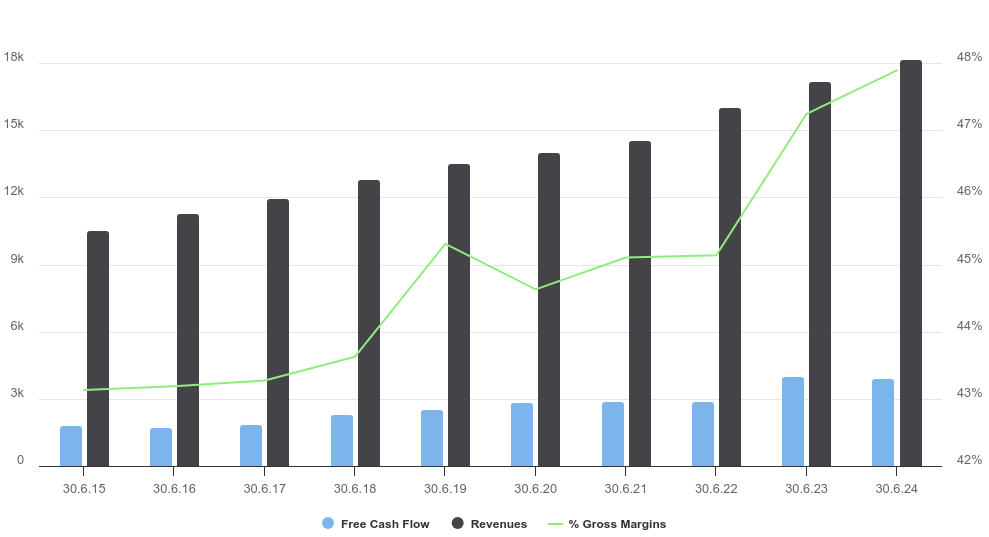

Don’t just take my word for it, look at the hard facts (revenue + fcf are in millions):

This isn't a flashy tech startup or a risky A.I. play. It's a rock-solid performer that's been quietly making investors wealthy for decades.

But only those who are “in the know”.

How? By doing what it does best - providing a critical service that many businesses can't function without - unless they want to pay hefty fines.

But here's the kicker: Despite its impressive track record, this stock is still flying under the radar of most investors.

That's where you come in.

In my latest report, I reveal:

The identity of this "sleep-well-at-night stock"

Why its business model is almost recession-proof

How recent legislation has strengthened its market position

Why businesses are forced to use their products - unless they want to get sued.

Don't let this opportunity slip through your fingers. While others chase the next big thing, you could be securing your financial future with a true market stalwart.

Click the link below to access the full report and discover the stock that could be the cornerstone of your portfolio for years to come.

P.S. In an era of uncertainty, this company offers something rare: predictability. Don't wait - learn about it now before the rest of the market catches on.

The rest is up to you.

Until the next issue. 👋

Appreciate my unique take on stock investing? Consider donating the price of a coffee to keep these insights coming:

If you enjoy The Onveston Letter, let me know by clicking the “Like” button ❤️.

And if you aren’t a subscriber yet, then sign up below to not miss out on future articles.

For new readers: Check out all my previous posts here

Disclaimer: This analysis is not advice to buy or sell this or any stock; it is just pointing out an objective observation of unique patterns that developed from my research. Nothing herein should be construed as an offer to buy or sell securities or to give individual investment advice.

Thanks for the short answer (no) at the top. Cutting right to the chase.