Mastering Dividend Returns: The Key Metric That Shapes Dividend Success.

What we Can Learn From The Cash Flow Statement

Dear Investor,

In this article, we'll dive into the world of cash flow statements and why they're key for dividend investors. Think of these statements as a diary that shows a company's cash earnings and spending over time.

If a company isn't increasing its cash each year, then there's a good chance the growing dividends you're hoping for might not last. So, for those keen on getting steady dividend increases, understanding this statement is a must.

Let’s get into it.

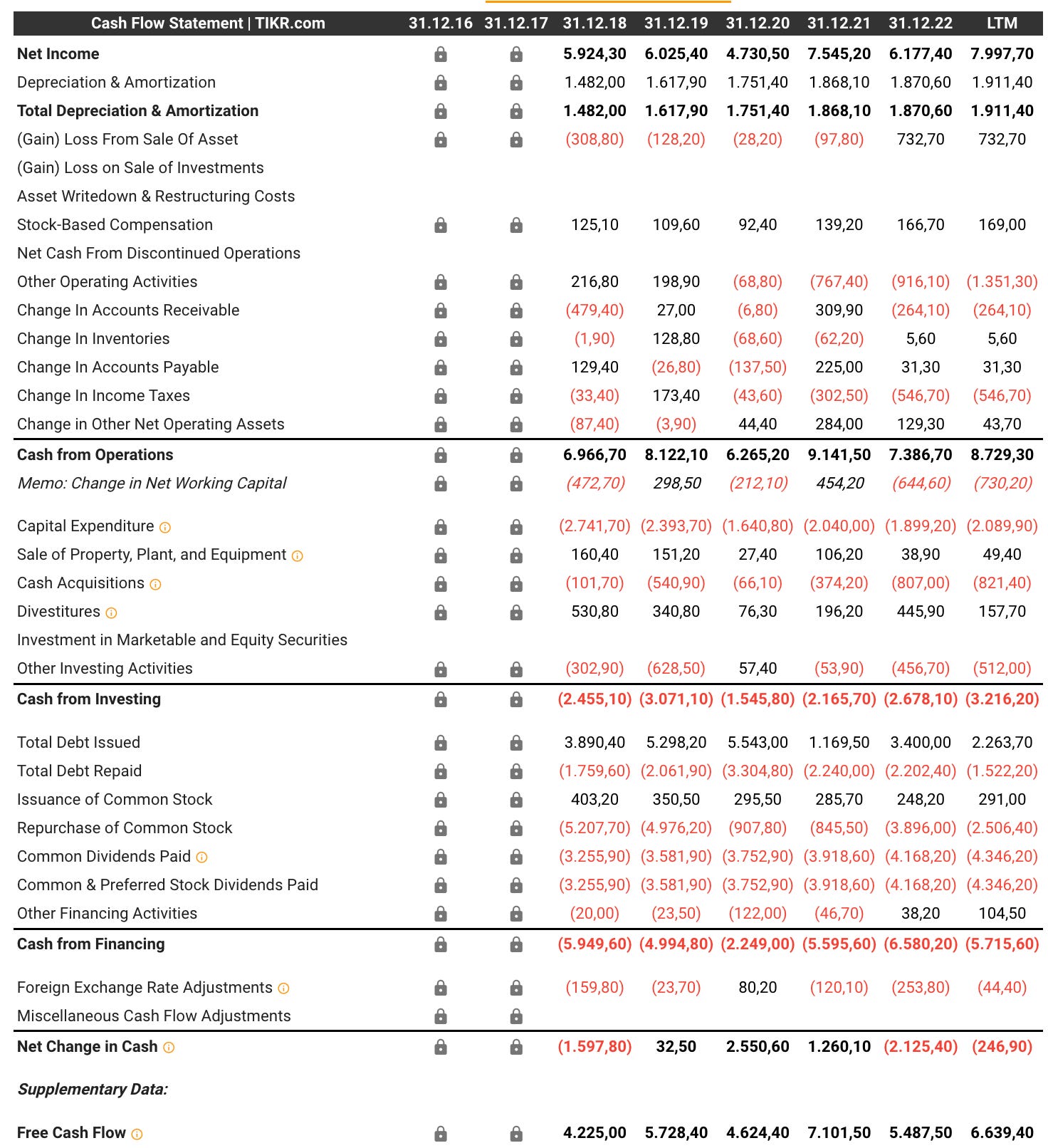

Cash is king when it comes to investing, as it reflects the overall health of a business. For illustration purposes, we’re going to use McDonald’s Corporation MCD 0.00%↑ as an example.

Below is their Cash Flow Statement from 2018 until today:

The 3 Types of Cash Flow Activity Are:

Cash from operating activities: This section describes the capital flows generated and expended for the normal operation of the business, including the short-term assets and liabilities. This includes the purchase or sale of inventory, alterations in accounts payable and accounts receivable, and operating expenses such as advertising.

Investing activities: This section focuses on the capital used or generated by long-term investments. This includes the purchase of buildings, equipment, and other long-term assets to maintain and expand the business, as well as the repair of outdated equipment. In addition, this section includes acquisitions and the sale of marketable securities.

Financing cash flow: This section describes the capital flows associated with paying down or incurring additional debt, issuing or repurchasing shares, and paying dividends.

Why is Cash so Important?

First off, having more cash means a company can easily pay off its short-term debts, which is essential for its health and growth. When this money pile keeps growing, it's a good sign, especially if you're hoping for growing dividends.

Another big plus of having cash? Flexibility. Say a golden chance pops up – maybe to upgrade old equipment or invest in new technologies. Companies with cash can jump right in! But if they're cash-strapped, they might miss out or rely on debt, making it hard for them to grow or even survive in tough times.

There's also the trust factor. While some financial figures can be dressed up to look better than they are, it's tricky to do that with cash flow. So, if you see a company consistently showing good cash flow, you can trust it more.

For those who invest for dividends, this matters big time. Steady cash flow hints that the company can keep paying – or even raise – those dividends. Always look for a long history of positive cash flow when picking dividend-paying stocks.

Cash from Operations

Using McDonald’s as an example, a positive operating cash flow indicates the company earns more than it spends in daily operations.

Let’s assume we don’t know the company behind those numbers (from $6.966,70 Billion in 2018 to $8.729,30 Billion in the last twelve months), we can still derive that the business must be stable with an upward trend and recurring customers.

However, if a company doesn't have a positive cash flow, it might resort to borrowing, which can be seen under the financing activities. For those looking to invest in dividend-paying companies, steering clear of businesses without positive cash flow from operations is a wise choice.

Cash from Investing

Encountering a negative number in this line is not a negative sign, it just means that the company is putting their money to work. Here are the last years of capital expenditures from McDonald’s:

Oftentimes you will find a different term for capital expenditures: "Purchase of property, plant and equipment (PP&E)," or something similar. Just be aware of that when looking it up.

Now you can use for those two numbers a simple Free Cash Flow formula to find out how well the business is running:

Free cash flow (FCF) = Net cash from operating activities - Capital expenditures (CapEx)

This brings us to the following numbers (in millions):

2018: $6.966,70 - $2.741,70 = + $4.225,00

2019: $8.122,10 - $2.393,70 = + $5.728,40

2020: $6.265,20 - $1.640,80 = + $4.624,40

2021: $9.141,50 - $2.040,00 = + $7.101,50

2022: $7.386,70 - $1.899,20 = + $5.487,50

In short:

McDonald’s Free Cash Flow is positive year after year.

A few things you should look out for when it comes to interpreting FCF:

A positive FCF.

Consistency (no huge up and down jumps because this could be an indicator that a business is not stable).

Ideally a bigger number each year (this indicates that the company is growing and has its spending under control)

No huge growth in capital expenditures (you see this often at the end of a market cycle when new companies go public and suddenly traditional valuation metrics don’t matter anymore; those companies have usually huge capital expenditures to fund their revenue growth - at the cost of profitability)

In summary, FCF serves as a robust indicator of a company's stock price trajectory over time. It can serve various purposes, from distributing dividends to shareholders to reducing debts, buying back company shares, or saving it for future investments - which all increase shareholder value over time and make a stock more attractive.

Cash from Financing

Companies lacking positive Free Cash Flow (FCF) often resort to debt to stay afloat. When you come across a company that is not only FCF negative but also growing its debt load year after year, you should never ignore this warning sign, no matter what Jim Cramer or Cathie Wood tell you. 😉

Poorly managed companies sometimes attempt to pay long-term debts with even more borrowed funds. This tactic may seem viable when interest rates remain low and credit flows freely.

However, when economic tides change, these companies find themselves vulnerable to higher interest rates and reduced credit availability. Consequently, if they fail to secure additional debt to cover their initial investments, bankruptcy knocks on the door, and the dividend often vanishes long before.

To check out the extent of McDonald’s debt obligations, one can delve into a line titled "Proceeds from issuance of debt," "Proceeds from debt," or a similar description within the financing activities section of the cash flow statement.

In the stock screener that I use for this example (Tikr), it’s called Total Debt Issued. 👇

(Note: Debt analysis is an extensive topic that requires a deeper understanding of accounting. I will cover this in future articles)

Final Words

Keep in mind that this article is just a simple introduction to the cash flow statement and the important pieces of information you can get out of it.

A more advanced way to calculate the “real” profitability of a company would take for example taxes into account since they are an additional expense that doesn’t land in the shareholders’ pockets.

There are many ways to skin a cat and if you don’t get bored by it and want more articles on financial analysis in the future (with stocks as examples and other metrics), let me know by clicking the Like ❤️ button.

Until the next issue. 👋

If you aren’t a subscriber yet, then sign up below to not miss out on future articles.

For the new readers: Check all my previous posts here

Disclaimer: This analysis is not advice to buy or sell this or any stock; it is just pointing out an objective observation of unique patterns that developed from my research. Nothing herein should be construed as an offer to buy or sell securities or to give individual investment advice.

A company like Amazon is an interesting example of FCF vs. profitability. For years, net income hovered around zero, yet the stock was price quite consistently on a multiple of 20-30x Cash from Operations (and still is today). And FCF was not necessarily great over that period either, as capex spending on warehouses and data centres remained high. So it seems like investors assumed that as long as CFO kept growing strongly, the capex would get good returns in the long run and were willing to invest even if net income and FCF weren't delivering yet today. I'd be curious to know your take on this one. Thanks!

Great summary of the CF statement. I agree that large one off capital expenditures can be a flag, but I think it's not always bad and sometimes it requires a deeper dive to understand what the investment is in and whether it's likely to generate good future return (based on both past performance and understanding the details). If a company has consistently good cash return on investment and the new project makes good business sense then the higher capex might be a good thing? And it's the same with acquisitions too I guess; whilst these don't impact the FCF it can equally destroy the cash left over for shareholders if done badly. (big spikes in acquisitions should be another flag when looking at a cash flow statement, under the investing section)