Passive investing is holding you back. There's a much better way.

Don't get lured in by promises of minimal work.

Hi Everyone,

passive investing is a concept that has become popular in the last decade among millennials and the early retirement movement. It refers to an investment strategy that does not rely on active management by the investor. That means that you do not make any changes to your investments based on market movements or changes in your financial situation.

For our purposes here, we will define passive investing as any strategy that seeks to achieve market returns by investing in index funds or ETFs rather than trying to beat the market by selecting individual stocks or managed funds.

In this article, I will attempt to spur readers to think critically about what the goals of the passive investment philosophy truly are and to what extent these goals are compatible with their own personal objectives. Because many of its vocal promoters don’t actually understand what this investment approach is designed to achieve.

The argument in favor of passive investing usually goes like this:

“After fees are deducted, active portfolio managers underperform the benchmark index. As a result, you are better off investing passively in a low-cost index fund that aims to mirror the performance of a benchmark index.”

So far so good. Who doesn’t want to avoid underperformance? Here’s the first problem with this approach: The aim of passive investing is articulated in terms of something to avoid rather than something to positively attain. Loss avoidance is great, but what is the actual goal? Is there any specific goal formulated that sounds reasonable AND suits the needs of investors? This brings us to the next problem: Mediocrity.

The term "mediocre" is not utilized in the literature that supports the passive investment strategy. In reality, average and random investment returns are the primary aim of the passive investing strategy. And this seems to be the best case possible. You won’t outperform. If you just keep buying an index fund you get the index funds returns, nothing more. Are you happy with mediocre results? And more importantly, do average results satisfy your demands?

“But Warren Buffet said that investors should dollar-cost-average in index funds.”

Yes and no. His advice gets often misquoted. He said that most investors are not able to generate any positive returns, hence it’s smarter for them to buy index funds so they get at least the market return. He never said that it’s the best approach, but that’s the best approach for those who have no idea what they’re doing (of which there are many, even in the professional space). However, he himself is still a stock picker simply because he can achieve superior returns. There’s no reason for him to buy index funds.

Can you actually achieve the average historic rate of return?

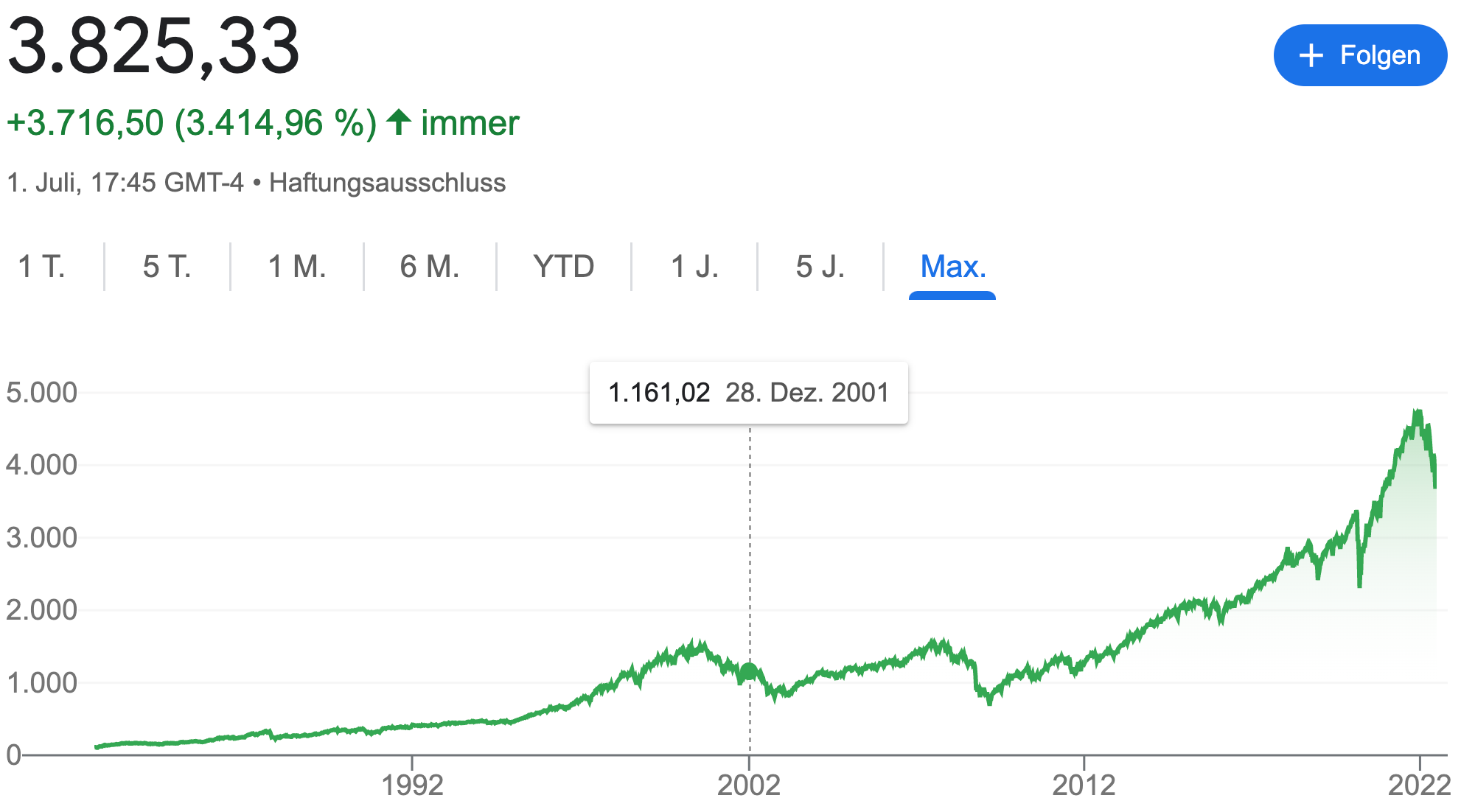

Many passive investors believe that the returns targeted by the passive investing method are the average returns earned by investors in the past. Well, yes you can assume that, but do you have a time horizon of 30 years to sit out a possible decade of underperformance? How do you know when to buy an index? In the best case, you use the average valuation metrics of all stocks the index contains, and even then this information is quite useless. With single stocks, you can lower your risk and get a more precise picture of what you actually buy. How are you going to do that with 500 random stocks, whose common denominator is their market cap? Let’s say you bought by the end of 2001 after the dot-com bubble burst. Ten years forward your portfolio would still have the same value. Are you really going to wait 20 more years to get the average 9% return that passive investing proponents strive for?

Keep in mind that in that timeframe investors get dozens of new opportunities: New companies, unjustified selloffs, undiscovered growth opportunities, etc. Do you really want to miss out on those gains just because financial bloggers told you that you shouldn’t even try because you will fail anyway and you should stick to passive investing? I’m not saying investing is easy, it’s not, but it’s simple as long as you follow a timeless and rule-based system.

“Mastering the boring basics in investing is how you become an expert.”

I already gave some examples of how to invest the right way in previous Newsletters and more will come in future ones.

Taxes and inflation

Let’s get to the next part that barely gets mentioned. And this is a huge disadvantage if you run the real numbers. Even if we take the “official” inflation numbers of around 3% you are left with an average of 6% gain per year. On top of that most index funds don’t pay a decent dividend so sooner or later you will be tempted to sell some shares. And depending on the country you live in you are obligated to pay capital gains tax.

Why do indexes actually rise?

Now we’re coming to the interesting part that leads us to a much better approach. Mistakenly the impression is created that index funds rise over time because the economy grows and the companies in the index perform well. Not so much. In fact, only a handful of stocks are the main drivers that lift the whole index up. Imagine you bought 10 stocks 10 years ago and one of them becomes a ten-bagger while the rest stay at the same price. Your portfolio has nearly doubled thanks to just one stock.

Let’s use a less extreme example. You don’t need to be a genius stock picker and researcher, all it takes is to avoid stupid mistakes and construct your portfolio in a way that the winners outweigh the losers. Let’s compare the performance of a stock we all know: McDonalds.

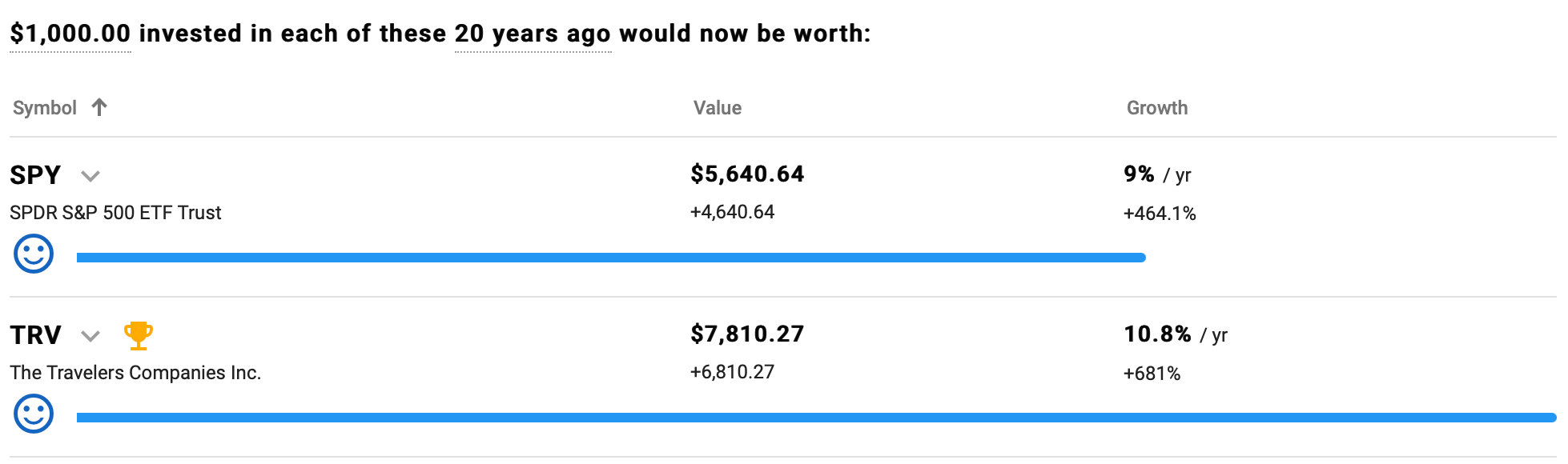

Keep in mind that McDonalds is not a spectacular Tech Stock. But still, a 15-bagger over 20 years is very impressive. 9% vs. 14.7% per year is a huge difference, so let’s check what a smaller difference would look like. A core part of my portfolio consists of insurance stocks, The Travelers Company is one of them:

Even 1.8% outperformance per year leads to tremendous results. A 5.6-bagger versus a 7.8-bagger. Now imagine how your whole portfolio could look like if you construct it in a way that the odds are in your favor and your money is not exposed to randomness that you have zero influence on.

I am currently writing a book/guide on how to create your own ETF that lets you sleep well at night and outperforms the benchmark. It’s based on a quantitative strategy that I developed myself and is tested with real money, not some theoretical backtesting method under optimal circumstances. Will give you an update and more details about it as soon as it’s ready. Those who are curious about my performance and found me outside of Twitter can follow me on Twitter.

Final thoughts

By the end of the day, you decide how you invest your money. My job is to provide you with viewpoints that you won’t find in mainstream financial media and that are based on personal experience and not on theory so that you have all the information you need to make sound decisions when it comes to your financial future.

“If you follow the advice that you hear on financial media but still get no significant results, there’s only one conclusion: The propagated methods don’t work.”

Hope you learned something today, until the next issue. 👋