Subscriber Letter #2: Is Automatic Data Processing A Value Stock Right Now?

Is AI a real threat to Automatic Data Processing or are the fears overblown?

Automatic Data Processing is one of the most “like clockwork” businesses out there. They’re essentially the world’s largest back-office helper. They handle the complicated paperwork, taxes, and payments that companies have to deal with so those companies can focus on their actual work.

As of early 2026, ADP serves more than 1.1 million clients in over 140 countries.

They pay roughly 1 in 6 workers in the U.S.. ADP’s biggest advantage is compliance. Tax laws and labor rules change constantly in every country. For a global company, it is much cheaper to pay ADP to keep track of those rules than to hire an army of lawyers in 140 different countries to do it themselves.

In their latest Q2 2026 report the company was reporting strong results.

Compared to last year’s second quarter, revenues increased 6% to $5.4 billion and 5% on an organic constant currency basis. Net earnings increased 10% to $1.1 billion, and adjusted net earnings increased 10% to $1.1 billion.

Adjusted EBIT increased 10% to $1.4 billion, and adjusted EBIT margin increased 80 basis points to 26.0%. ADP’s effective tax rate for the quarter was 23.2% on both a reported basis and an adjusted basis. Diluted EPS increased 11% to $2.62, and adjusted diluted EPS increased 11% to $2.62.

On top of that shareholders are getting rewarded with higher dividends and a new share repurchase program:

“We are also raising our fiscal 2026 adjusted EPS growth forecast to 9-10%, supported by share repurchases. Earlier this month, out Board authorized the purchase of $6 billion of out common stock, which replaced in its entirety our 2022 authorization of $5 billion. This new authorization, along with our recent 10% dividend increase signals out continued commitment to driving shareholder value and to returning excess cash to our shareholders, which remains a key pillar of our capital allocation strategy.”

- Peter Hadley, CFO -

Furthermore, the company’s underlying efficiency remains exceptional, boasting a Return on Equity (ROE) of nearly 74% and a Return on Invested Capital (ROIC) of 50%.

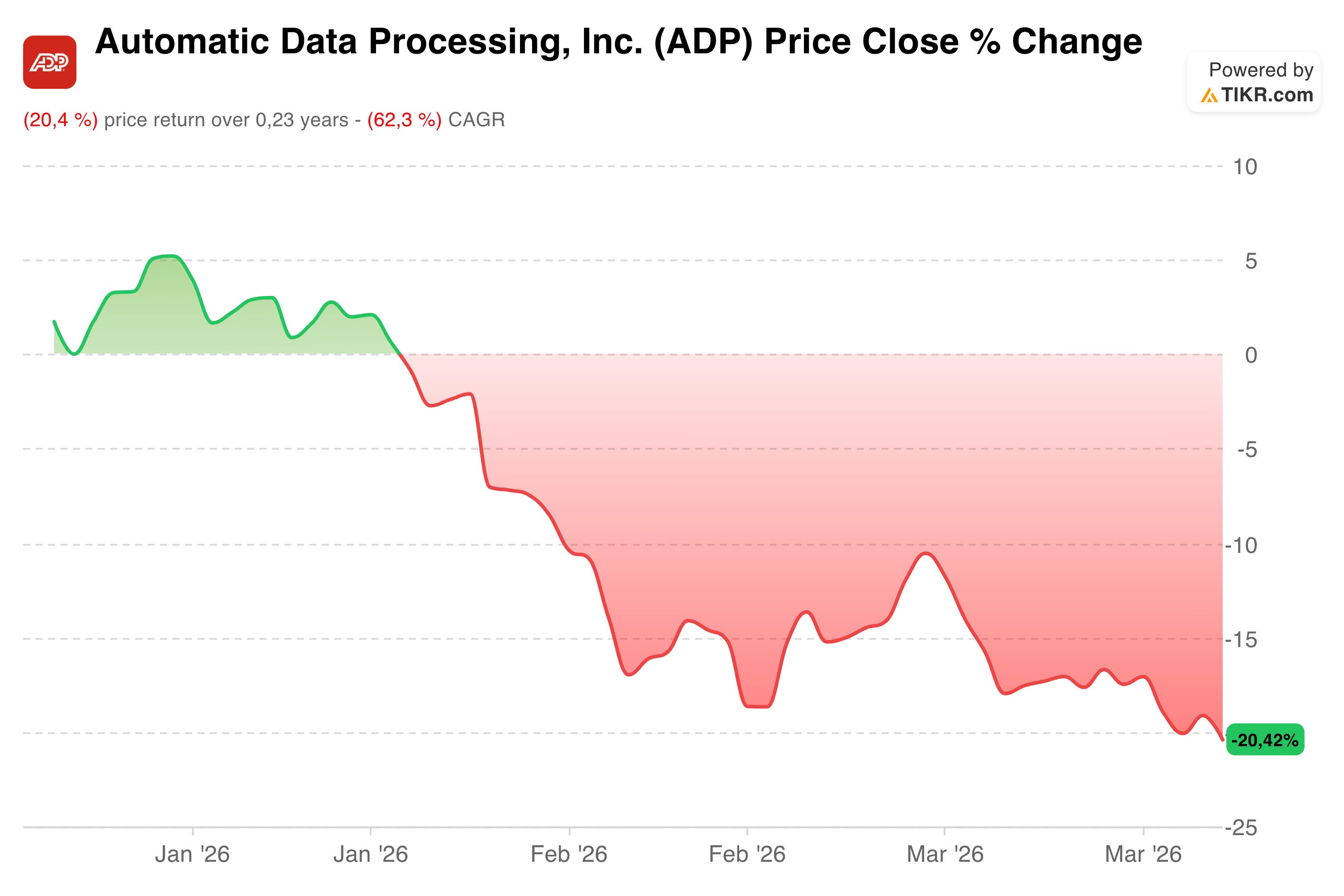

Despite these stellar fundamentals, the stock has pulled back 20% YTD. This disconnect is driven by market anxiety regarding AI-led disruption and the looming threat of mass layoffs, both of which investors fear will erode the bottom line.

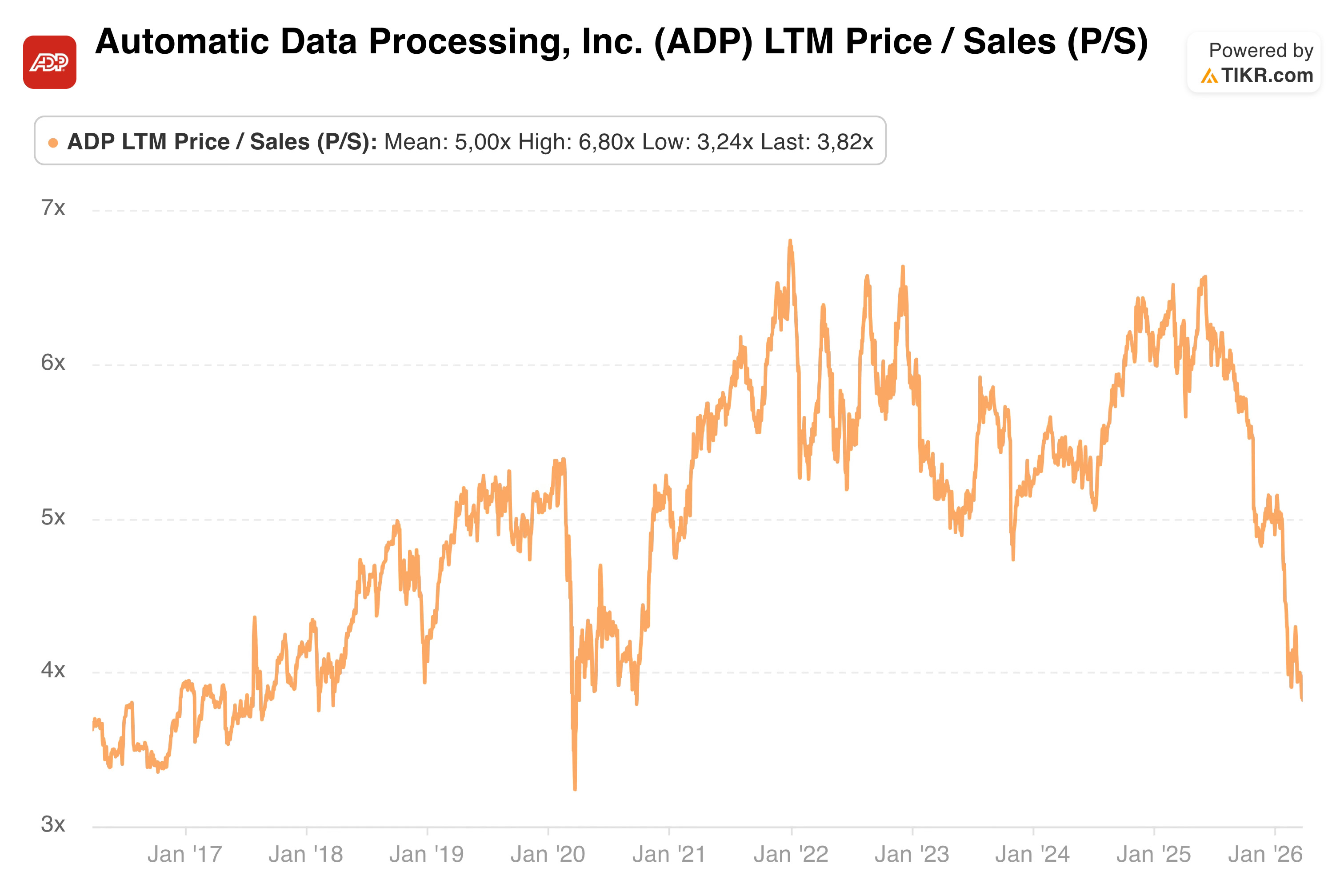

In addition to the 20% YTD decline, ADP is now trading at a Price-to-Sales (P/S) ratio of approximately 3.8. To put that in perspective, the market hasn't offered a valuation this attractive since the 2020 pandemic crash, a period when the global economy was at a complete standstill.

This suggests that the current 'AI fear' is being priced with the same severity as a total economic shutdown.

But here is the billion-dollar question: Is AI a disruptor that will automate ADP into irrelevance, or is it the ultimate margin-expansion tool for a company that owns the world’s largest dataset on human labor?

Wall Street is split: half see a 20% discount on a blue-chip compounder, the other half see the early innings of a slow-motion disruption. After digging through the filings, the earnings calls, and the competitive landscape, I think both sides are missing the bigger picture.